During this project, JAI permanently took out a sizeable chunk of expenses and fixed costs from their business (we estimate Rs 500-600mio). They achieved this by streamlining and modernizing manufacturing practices, cutting interest costs deleveraging their balance sheet by becoming net-cash and optimization of plants and manpower. Because of their continuous cost reduction efforts, at the end of FY20, their break-even utilization was down to < 40% and < 33% in FY20 and FY21 respectively. These efforts significantly increased their ability to weather the storm caused by the covid-19 pandemic and they were able to bounce back to profitability with only a slight recovery in the overall commercial vehicle sales.

Given that the aftermarket opportunity can be as large as supply to OEMs, JAI has significantly improved its reach and capabilities to grow aftermarket sales. They have continuously invested in technology to better manage the entire supply chain as well as build dealer connect and loyalty which will enable them to not only garner better margins but diversify their income stream and grow faster than the underlying CV sales.

Starting FY21, JAI has embarked on Lakshya 50XT, their first five-year plan with the objective to achieve future growth and to de- risk business further through market & product diversification. The FY’26 targets for Lakshya 50XT are: (1) 50% revenue from new markets with 10% revenue from new export markets; (2) 50% revenue from new products like allied suspension, machined parts, full range of trailer suspension and other products; (3) 50% return on capital employed and (4) 50% of profits distributed as dividend.

Jamna is working towards adding multiple new products which will increase their content per vehicle. This should help achieve better growth and higher margins. The management have demonstrated the ability to put a more variable cost structure in place, significantly reduce breakeven to ~25% now (from ~40% a few years ago). By funding capex through internal accruals, the company now has a robust net cash balance sheet.

Our unwavering preference and focus for quality remain intact no matter the cyclicality of the industry. We like to invest in businesses and management teams which are driven, leaders in their segment and can transform themselves in tough times. Companies which help themselves by getting into more value-added and add adjacent products with a strong balance sheet can help mitigate a downturn. We think as JAI moves towards achieving its medium-term goals, the volatility in the business can reduce further and it will emerge stronger in each subsequent cycle. Jamna is very well placed to take advantage of the CV cycle for the next few years.

Market & Performance Update

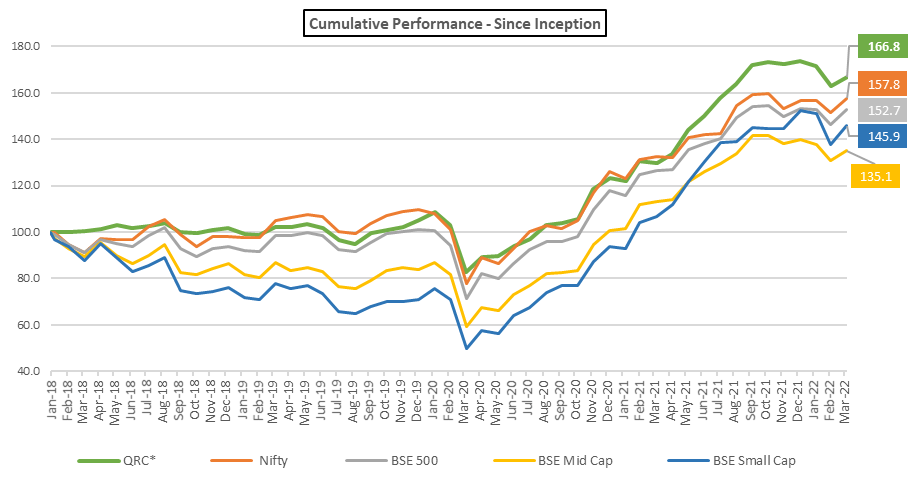

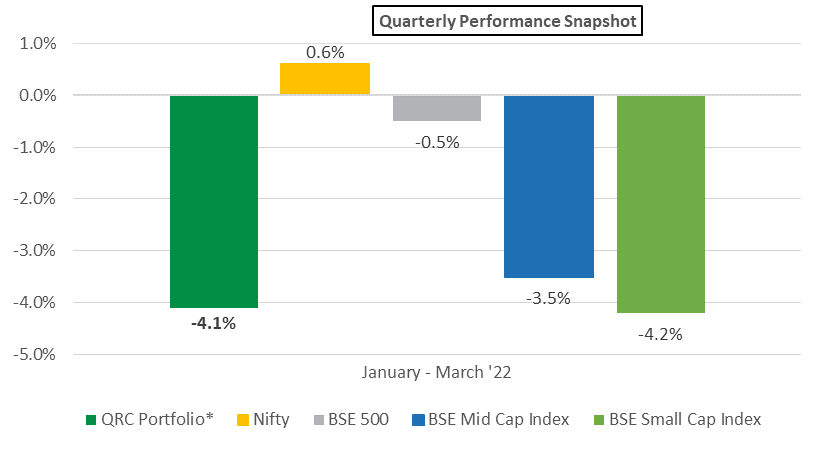

For FY22 (April 2021 to March 2022), the QRC Long Term Opportunities Portfolio (LTOP) was up 28.5%. Our 1-year return for the period January 2021 to December 2021 period was 41%. The markets have been consolidating in a range over the last six months as participants are grappling with the ever-resetting inflationary expectations and the quantum of rate hikes from the US Federal Reserve. The onset of the Russia-Ukraine war has resulted in significant jump in commodities across the board and aggravated the already persistent supply chain concerns. The March quarter saw the benchmark Nifty index gain a paltry 0.6%. while the small and mid-cap indices were down 3-4% each.