Dear Investor,

We hope this letter finds you and your loved ones safe and healthy. We have witnessed one of the steepest falls and the fastest recovery in the history of global equity markets in these past few months. This time last year, we were looking at the Indian economy on the cusp of a recovery, albeit a slow one post the corporate tax cuts and other measures taken by the government. The economic impact of the covid-19 related shutdown seems to suggest that the Indian economy will likely de-grow by >10% for FY21 and with the right stimulus, support, and measures, will bounce back by 8-10% for FY22.

Performance Update

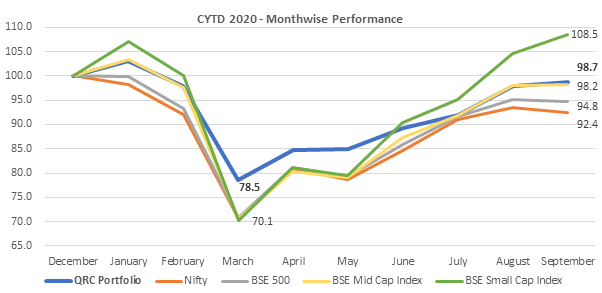

For the 1st Half of FY21 (April to September 2020), the QRC portfolio was up ~26% but despite this strong performance it lagged the major market indices which have bounced sharply since their lows in March. Unprecedented global liquidity and easy monetary policy with the promise from Central Bankers to do ‘whatever it takes’ resulted in the US markets bouncing back to new all-time highs despite the economic challenges. This momentum spread to the other global markets including India. Small cap companies which had been major laggards over the last 2+ years bounced back the hardest.

*Individual client portfolio returns may differ based on timing of their investments and specific instructions/circumstances. QRC returns are TWRR. Source: BSE & NSE

To put the performance in perspective and get a better sense of how volatile and choppy markets have been, it is important to zoom out and take a slightly bigger picture view. Markets fell nearly 30% from their January highs. Assuming a starting value for the portfolio (and indices) at 100 at the end of December 2019, the QRC portfolio was already well within touching distance of parity at 98.7 by the end of September 2020 (chart above). In the early days of the pandemic we assessed that a few of the businesses we owned could be under pressure and have a more back-ended recovery. As a matter of prudence, we exited those positions and raised more cash by trimming some of our other holdings as well given the heightened state of uncertainty then. As a result, QRC outperformed the major indices like Nifty and BSE 500 (more representative of our portfolio currently) by a ~4-6% during CY20 till date.

Markets have shown a lot of resilience since May’20 and nearly recovered in a ‘V’ shape as investors began to treat 1QFY 21 as an exceptional quarter and have continued to look ahead to more normalisation by 3QFY21. By the end of September 2020 and the time of this letter, we have deployed significant amount of the cash raised and have added some high quality names in the portfolio (sectors like autos, IT services, healthcare etc) which we think provide very good risk adjusted opportunities.

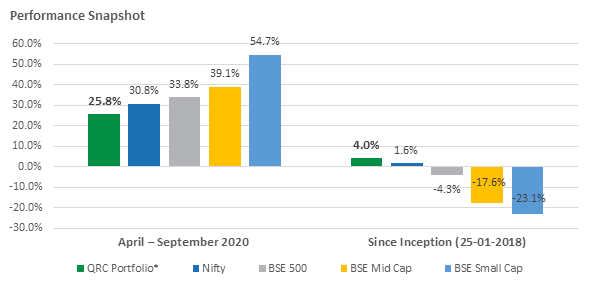

As we have highlighted earlier, we run a benchmark agnostic portfolio and our endeavour is to buy and own quality businesses (no matter the sector or market capitalization) at a good price as we believe, a good quality business will consistently perform better across business and economic cycles and not just when there are economic and liquidity tailwinds. A snapshot of QRC’s 1HFY21 and since inception performance validates the same with the QRC portfolio outperforming all the major indices since its inception in January 2018. While the small cap index’ bounce of ~55% in 1HFY21 looks stark, the index is still down 23% on a three year basis and has ground to cover to return to parity.

*Absolute returns. Individual client portfolio returns may differ based on timing of their investments and specific instructions/circumstances. QRC returns are TWRR. Source: BSE & NSE

Portfolio Snapshot

| Top 5 Holdings* |

|

Market Cap Split* |

|

| Tata Consultancy Services |

6.0% |

Large Cap |

41% |

| Britannia |

6.0% |

Mid Cap |

12% |

| Suprajit Engineering |

6.0% |

Small Cap |

33% |

| Marico |

5.0% |

Cash & Equivalent |

14% |

| Alkem Laboratories |

5.0% |

|

|

*Illustrative. Individual client portfolios may differ based on timing of their investments and specific instructions/circumstances.

Looking Ahead

Policy makers’ actions on loan moratorium, economic stimulus as well as support for SME businesses have put a floor on economic activity. Going into the Indian festive season of October/November life does seem to have returned to normal. Businesses have tightened their belts and taken aggressive cost cutting measures especially around discretionary spending like advertising/promotions. In some cases, covid-19 may have permanently taken some portion of costs out of the business like travel/meetings/conferences etc and all this combined has meant that companies were able to show robust margins in the results of quarter ended September 2020 despite lower revenues. While some of these cost savings will not be permanent as normalcy is restored, we believe that we are in a period of higher margins at least for the next few quarters as some of the efficiency gains will be retained. A lot of our businesses may achieve much higher profits even as revenues come back to pre-covid levels as they benefit from operating leverage.

While there is ample global liquidity and local interest rates continue to remain supportive, we do not think one can lower one’s guard as some of the easing measures taken by the government and RBI will likely be eventually reversed. Government’s fiscal deficit remains a tight rope walk, and we believe that one cannot rule out the possibility of higher taxes as government finds ways to fund its fiscal stimuli. We are enthused by the various ‘Atmanirbhar’ policies like Production Linked Incentive (PLI) introduced by the government as this will go a long way to address what we believe is the key problem in India – youth unemployment.

We are running a slightly more diversified portfolio now given that uncertainties around a second wave of covid and hence sporadic lockdowns remain. We have added some quality cyclical names that should benefit from a normalisation and pick-up in economic activity over the next 12-18 months. Our portfolio remains a balanced mix of Large and Small/Mid cap companies where we think business owners/managers are making the right strategic decisions from the mid to long term view. We believe we are at the beginning of the next economic cycle over the next few years and remain enthused by the prospects of our investee companies’ growth opportunities.

We thank you for entrusting us with your money. Do feel free to reach out to us with your questions or suggestions.

Sincerely,

Saurabh