Dear Investor,

Stock Market Update

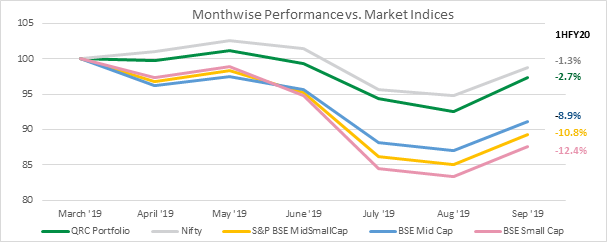

The first half of financial year 2019-20 has been very eventful with India having its fair share of headline grabbing developments. From a resounding re-election of Narendra Modi and BJP to a very uninspiring budget session in parliament followed by backlash from industrialists to a host of economic reforms – we have seen it all in the past few months. The markets initially cheered the BJP victory but were quickly disappointed by a slew of ‘socialistic’ measures adopted by the new Finance Minister which included raising taxes for the super-rich & tinkering of regulations on foreign investments. What also stood out in the budget was the lack of any fiscal impetus for the economy to spur growth along. July and August of 2019 saw the Indian equity markets lose significant ground with market indices losing between 6 to 12%.

September finally saw some respite with the government announcing a significant tax reform. Indian base corporate income tax rate was cut from 30% plus surcharge to 22% plus surcharge. To spur fresh capital expenditure, new companies set up for manufacturing may pay income taxes as low as 17%. The government also announced measures to ease system liquidity and lower interest rates. The RBI continued on its path of cutting interest rates with a cumulative reduction of 110bps since March ‘19.

Global markets had their fair share of developments too. Brexit discussions and plans are still not finalised with the UK now set to have a general election in December’19. Trade tensions between USA and China seem to have eased a bit with some constructive dialogue but a deal is yet to be finalised. Political tensions between China and Hong Kong continue to weigh on sentiment. The EU continues to struggle with a lack of growth and interest rates continue to remain at 0%. US Fed also lowered interest rates by 50bps during the last six months. As a result, we now have ~$17 trillion of global bonds trading at negative rates vs. ~$10 trillion in March 2019 – which means that at maturity of these bonds, savers are happy to get less money back than what they invest today.

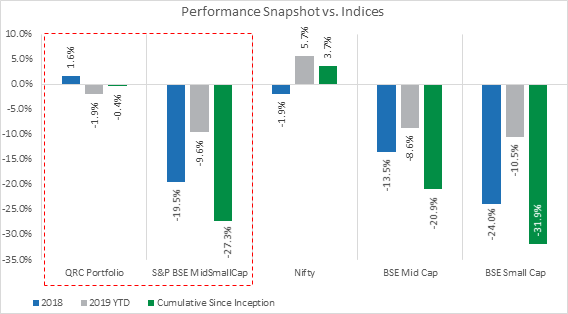

Against this backdrop, the QRC portfolio lost 2.7%* during 1HFY20. Nifty fared slightly better with a loss of 1.3%. The mid and small cap indices were down between 9% and 12% during the same period. Foreign investors sold nearly INR300bn of shares during the months of July & August. The recent sharp slowdown has resulted in a further narrowing of breadth in the markets. Investors continue to pay premium valuations for a small set of companies which are delivering in a growth challenged environment.

*Individual client portfolio returns may differ based on timing of their investments and specific instructions/circumstances. QRC returns are TWRR.

Source: BSE & NSE

| Key Sector Exposure* |

|

| Banks & Financials |

20% |

| Consumer Staples |

18% |

| Retail/Realty |

12% |

| Building Materials |

8% |

| Auto Ancillaries |

8% |

| Top 5 Holdings* |

|

| HDFC Bank |

6% |

| NESCO |

6% |

| Kotak Mahindra Bank |

6% |

| Phoenix Mills |

5% |

| Jyothy Laboratories |

5% |

*Illustrative. Individual client portfolios may differ based on timing of their investments and specific instructions/circumstances.

Reflection on Our Investment in Phoenix Mills Ltd

Phoenix Mills Ltd (PML) has built one of the leading malls in India on a legacy textile mill land in central Mumbai. Building on that success, in 2007, the company issued fresh equity to set up five similar retail-led mix-use projects which were completed by the middle of this decade. Over the last four years, the company has undertaken a host of other value accretive initiatives by investing Rs15bn from internal cashflow to buy out large PE investors from its JVs in a series of transactions. This resulted in PML taking its ownership to 100% in the three city centric mall projects in Mumbai, Pune & Bengaluru and to 50% in Chennai. These acquisitions were done at attractive valuations considering the PE investors’ time pressed desire to exit.

In August 2017, PML partnered with a Canadian pension fund who invested Rs16bn for a 49% stake in only their Bengaluru project valuing the joint venture at a post money enterprise value of Rs38bn. This valuation implies an 8x appreciation on the initial equity invested by PML in 2007-08. During 2017-19, this JV company has acquired three land parcels (Bengaluru, Pune & Indore) and is building similar retail led projects. PML itself has made two additional investments – acquired a semi-completed mall project from creditors in Lucknow. It has also jointly acquired a land parcel in Ahmedabad to set up its luxury Palladium mall. With these growth plans in motion, over the next four years, the total operational retail asset base could double (from 6mn sqft currently) and office asset base could quadruple (from 1.3mn sqft currently). The company has indicated that it still has enough room to add a few more assets in major cities at the right time and valuation. PML has achieved 9-10% revenue growth and about 18% profit growth on a compounded basis over the last four years. This growth is highly credible considering ongoing challenge to core mall business from e-commerce and the recent consumption slowdown in India.

We believe the company can grow its revenues & profits from its operational assets by 12-15% driven by underlying consumption growth and the rental renewal schedule. In addition, the five ongoing mall and office projects add further growth visibility to its recurring revenue businesses. With REIT regulations now firmly in place, PML has another avenue to raise growth capital and/or monetize assets. Key risks that we continue to monitor are cost and timely completion of projects and the ongoing evolution of e-commerce in India. We however note that there is already an incremental shift towards food & beverage and entertainment outlets within large retail formats.

Looking Ahead

The government seems to have clearly recognized the slowdown and taken steps to improve the mood in the economy. The corporate tax reforms should aid post tax profits of companies by 10-15%. Companies may choose to return this to shareholders (via dividend or buy backs) or re-invest it in their businesses to grow sales – either of the outcomes (if well executed) should be well received by the markets. We are at the 1-year anniversary of IL&FS default and will be lapping a low base of growth for the next four to six quarters. For the more short-term focused investors, this should improve growth numbers (optically) and could lend support to markets. October has started on a happy note for the markets with broad based buying witnessed and festive season sales across most categories doing better than feared. We had mentioned in our August Market Musings Letter, “We sense that fear is fast spreading and it is time for us to start feeling greedy.” True to form, we have added four new positions to the portfolio in consumer staples, financial and pharmaceutical sectors and rationalised our position in three holdings. We have also continued to deploy additional money in our existing holdings and together, have increased equity exposure by nearly forty percent over the last few months. While times remain challenging, we are far more comfortable and confident of stock valuations now. Our portfolio has a good mix of steady compounders and stocks that should benefit from an eventual economic recovery. The search and endeavour to find quality businesses at reasonable valuations continues.

We thank you for entrusting us with your money. We would love to hear your questions or suggestions.

Sincerely,

Team QRC