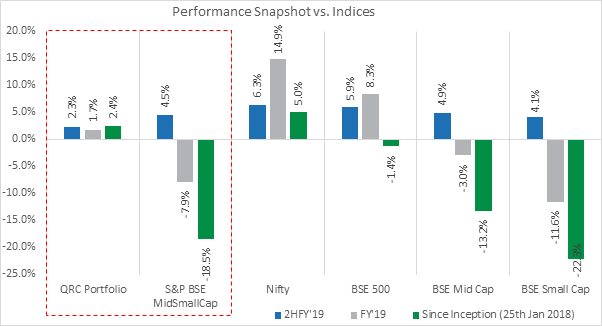

*Individual client portfolio returns may differ based on timing of their investments and specific instructions/circumstances. QRC returns are TWRR.

QRC Portfolio Key Sector Exposure*

| Banks & Financials |

12.5% |

| Consumer Staples |

11.5% |

| Retail/Realty |

7.7% |

| Media |

6.9% |

| Auto Ancillaries |

5.4% |

*Illustrative. Individual client portfolios may differ based on timing of their investments and specific instructions/circumstances.

Fine Organics Industries Limited

We started building a position in Fine Organics (FOIL) after its IPO in mid-2018. FOIL is a specialty chemical manufacturer operating in the high-end oleo-chemicals space (use vegetable oil as base vs. most others using petrochemicals). The company was founded in 1970s and till date, has not raised outside equity – showing astute capital allocation and measured expansion through internal accruals and promoter funding. The IPO was a liquidity event for the owner families to monetize some of their holdings via an 100% offer for sale. Over the years, the company has diversified from being just a food additive player to plastic additives and is the largest slip additive manufacturer in the world today.

FOIL’s key strengths are its ability to set up capacity at an estimated 1/5th to 1/8th the cost of global competitors given its very experienced in-house project team – this team also continuously helps the company in maintenance as well as process optimization. FOIL has a diversified client base spread over 70 countries with the largest client being <5% of sales. The additives that FOIL supplies form a very small proportion of value & weight of the final product but are very important for the quality/texture of the end-product. Given this, product approval cycles can be 2-3 years in some cases and once a supplier is selected, clients tend to remain sticky. Also, the fact that the additives are a very small component of overall cost for the client, FOIL can pass on cost increases (albeit with a bit of lag). FOIL runs a state-of-the-art research laboratory in Mumbai where they can conduct pilot tests which enables them to be a part of the product development conversation with the client from a very early stage.

FOIL is amid a capital expansion cycle through multiple projects that will nearly double its production capacity over the next three years. Typically, when a company undertakes large expansion, the stock price performance tends to falter as the markets worry about higher leverage and execution challenges. In the case of FOIL, we take comfort from their execution and capital allocation history as well as a strong balance sheet and cash-flows.

All in all, given these strengths, we believe that FOIL could be a steady compounding stock over the years as they increase capacity in the faster growing food additive business and monetise their work in the animal feed additive space. The key risks we will be monitoring are raw material prices & supplies given their largest supplier is nearly 30% of requirement and execution & ramp up of the expansion projects.

Looking Ahead

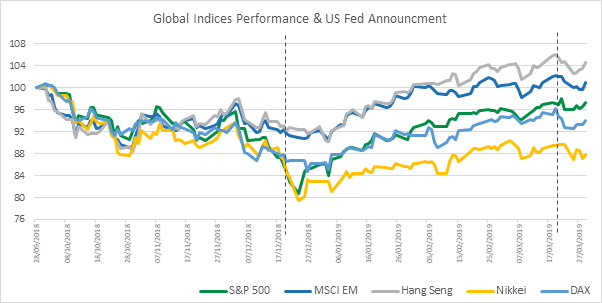

While the near-term focus of the market will continue to remain on the general election results, global growth, Brexit and the outcome of the trade wars and talks between China and USA, at QRC, we continue to look for individual stock ideas that fit in our philosophy and process. We have steered clear from businesses that overly rely on government policy and believe that barring a growth shock in India, all our companies should continue to build on their strengths and grow at a comfortable clip. In fact, after the sharp correction in the small and mid-cap stocks (our major area of focus) seen during 2018, we are far more comfortable with valuations and are increasing our exposure. To that end, we have added four new names to the portfolio in sectors like financials, media, consumer staples and building materials with no exits since September 2018. We remain confident of our holdings and the respective management teams to weather any global and/or local slowdown and continue to make strong decisions on an ongoing basis for the businesses and allocate capital efficiently. We have continued to deploy more monies into quality names and will continue to invest at levels and prices where we find risk-reward justifies our action. Post nearly half a decade of tepid earnings growth for the Indian benchmark indices, we think a recovery in earnings is closer than before and remain hopeful of stronger GDP growth in India once a new stable government is formed.

We thank you for entrusting us with your money. We would love to hear your questions or suggestions.

Sincerely,

Team QRC